Showing 1–20 of 437

-

Bio-based Building Blocks and Polymers – Global Capacities, Production and Trends 2025–2030 (PDF)

NewMarkets & Economy

23 Pages

1174 Downloads

1174 Downloads

2026-02

FREE

Free Shipping1174

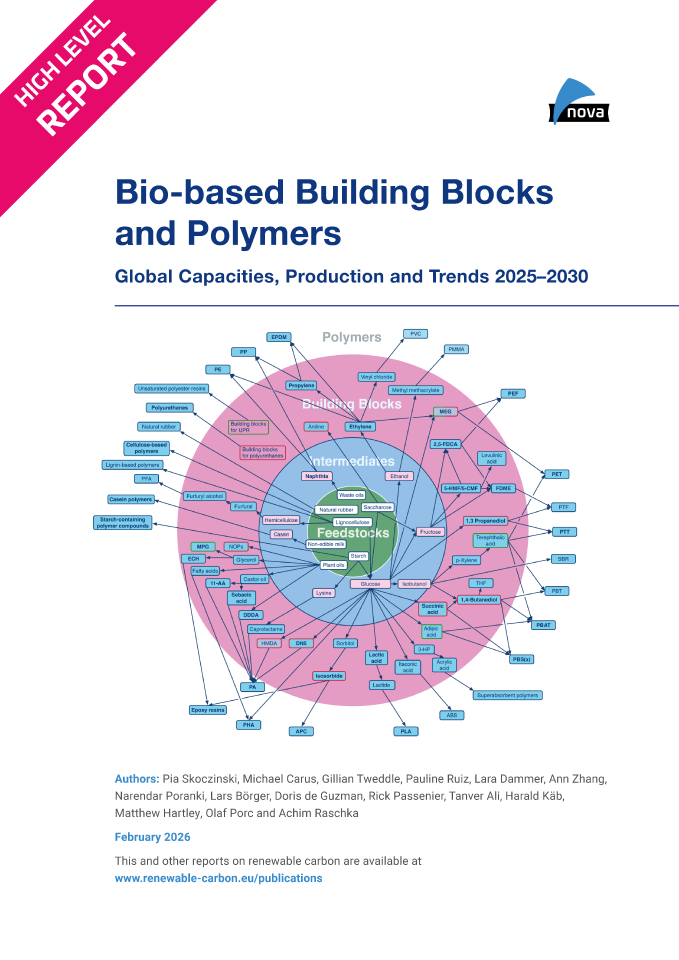

DownloadsThe new high-level report “Bio‑based Building Blocks and Polymers – Global Capacities, Production and Trends 2025–2030”, compiled by the international biopolymer expert group of the nova-Institute, provides an overview of the capacities and production data of 17 commercially available bio‑based building blocks and polymers in 2025, along with a forecast for 2030. Detailed market data is available via individual workshops and webinars with the biopolymer experts. This data includes capacity development from 2018 to 2030, production data for the years 2024 and 2025, and analyses of market developments per building block, polymer and producers, as well as a statistical analysis of “Mass Balance and Attribution (MBA)” products available worldwide.

2025 was a solid year for bio-based polymers, with an expected overall CAGR of 11 % to 2030 and an average capacity utilisation rate of 86 %. Overall, bio-based non-biodegradable polymers have larger installed capacities and higher utilisation rates than bio-based biodegradable polymers. While 58 % of the total installed capacities are from bio-based non-biodegradable polymers, 42 % are bio-based biodegradable polymers. Bio-based non-biodegradable have an average utilisation rate of 90 % whereas bio-based biodegradable polymers have an average utilisation rate of 81 %. The expected CAGR for both, bio-based non-biodegradable and biodegradable is similar with 10 % and 11 %, respectively.

Epoxy resin and PUR production is growing moderately at 9 and 8 %, respectively, while PE and PP are increasing by 17 % and 94 %. Also, capacities for the biodegradables PHA and PLA are expected to increase until 2030 by 49 % and 16 %, respectively. Commercial newcomers such as casein polymers and PEF have increased production capacity and are expected to continue to grow significantly until 2030.

DOI No.: https://doi.org/10.52548/PILO4285

-

Mapping of Global Advanced Plastic Recycling Capacities (PDF)

NewMarkets & Economy, Policy, Technology

35 Pages

2025-11

500 € – 1,000 €Price range: 500 € through 1,000 € ex. tax

Plus 19% MwSt.Press

release Select

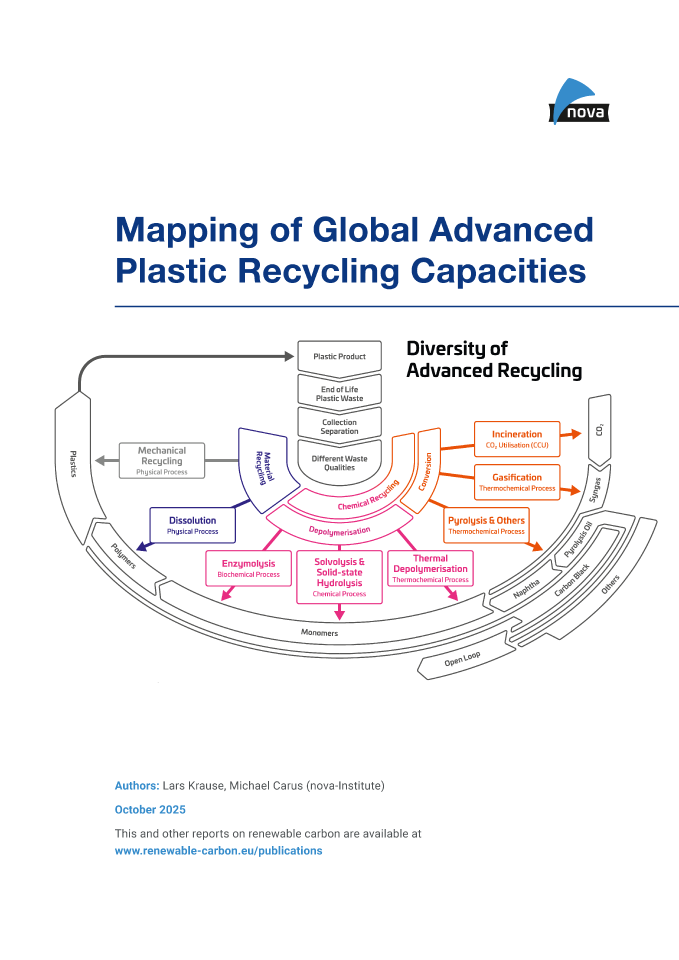

licenceChemical and physical recycling are essential to keeping carbon in the loop and fully establishing a circular economy. Despite delays in policy regulations and investment, experts foresee a bright future for new capacity, both globally and in Europe.

The development of advanced recycling technologies is very dynamic and at a fast pace, with new players constantly appearing on the market, from start-ups to chemistry giants and everything in between. New plants are being built, and new capacities are being achieved. Due to these dynamic developments, it is difficult to keep track of everything. The nova report “Mapping of global advanced plastic recycling capacities” aims to clear up this jungle of information. A comprehensive evaluation of the global input and output capacities was carried out for which 390 planned as well as installed and operating plants including their specific product yields were mapped to provide an overview about global advanced recycling capacities in the past, present, and future.

Further information: The new report represents a short study updating the current and future Advanced Recycling input- and output-capacities for the year 2024-2031. The report does not include any technology- or company-profiles which are published in another study (https://doi.org/10.52548/WQHT8696).

DOI No.: https://doi.org/10.52548/YKWB6074

-

Bio-based Building Blocks and Polymers – Global Capacities, Production and Trends 2024–2029 (PDF)

NewMarkets & Economy

434 Pages

2025-03

3,000 € – 10,000 €Price range: 3,000 € through 10,000 € ex. tax

Plus 19% MwSt.Press

release Select

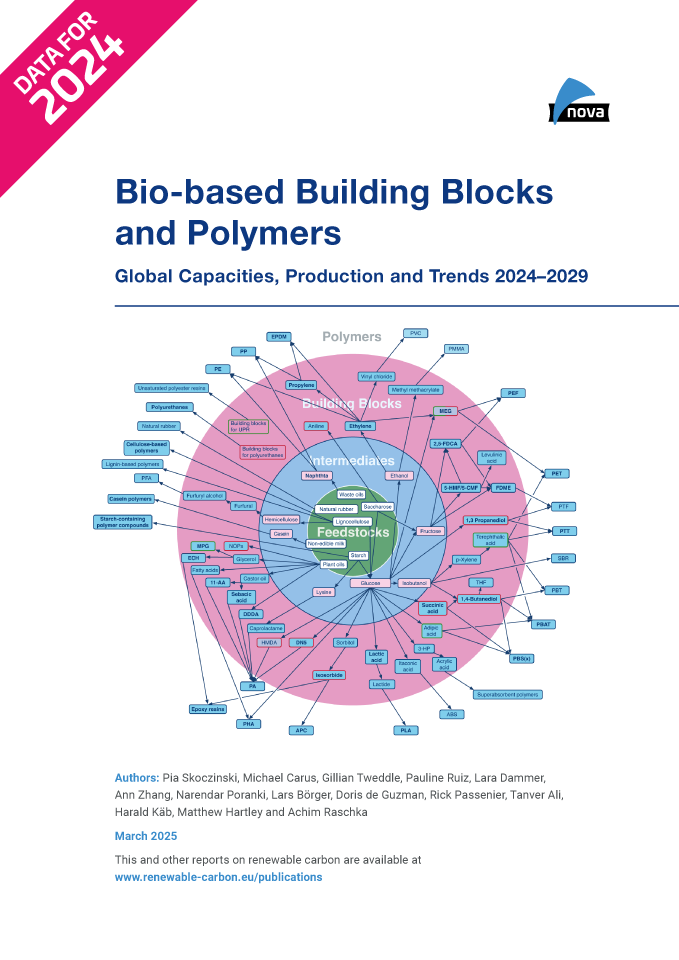

licence2024 was a respectable year for bio-based polymers, with an overall expected CAGR of 13 % to 2029. Overall, bio-based biodegradable polymers have large installed capacities with an expected CAGR of 17 % to 2029, but the current average capacity utilisation is moderate at 65 %. In contrast, bio-based non-biodegradable polymers have a much higher utilisation rate of 90 %, but will only grow by 10 % to 2029.

Epoxy resin and PUR production is growing moderately at 9 and 8 %, respectively, while PP and cyclic APC capacities are increasing by 30 %. Despite a decline in production of biodegradables, especially for PLA in Asia, capacities have increased by 40 %. The same applies to PHA capacities. Commercial newcomers such as casein polymers and PEF recorded a rise in production capacity and are expected to continue to grow significantly until 2029.

DOI No.: https://doi.org/10.52548/UMTR4695

-

Could the production of European chemicals be achieved without naphtha and steam crackers? What alternative pathways could be viable in the future? (PDF)

Markets & Economy, Policy, Technology

7 Pages

113 Downloads 113 Downloads

2026-05

FREE

Free Shipping113

DownloadsOver the next few decades, naphtha steam cracking will remain the dominant and most efficient process in the European chemical industry. However, naphtha is produced from crude oil, which is linked to several problems: (1) climate change, especially from Scope 3 emissions; (2) a linear instead of a circular economy; (3) most innovation taking place in other areas than crackers; (4) a failure to achieve resilience and strategic autonomy; and (5) Europe’s inability to compete with other regions of the world that have better access to cheaper crude oil and naphtha. Furthermore, (6) renewable naphtha produced from biomass, waste or CO₂ is very expensive (2–3 times more expensive), and (7) other pathways than naphtha and steam crackers are often more efficient for these alternative renewable feedstocks.

These are seven good reasons to discuss what alternative pathways could be viable in the future of Europe’s chemical industry and how they could be implemented. This paper mainly focuses on methanol, ethanol and biodiesel. Before delving into these topics, two brief comments on ammonia production, biotechnology and biomanufacturing and electrochemistry are provided.

-

Investments totalling more than 5 billion with a future bio-based quota for plastics in Europe (PDF)

Markets & Economy, Policy

3 Pages

70 Downloads 70 Downloads

2026-05

FREE

Free Shipping70

DownloadsImplementing a 5% bio-based quota for all polymers produced in Europe could be just as successful as the introduction of biofuels.

As a draft scenario, we assume that (1) 30% will come from bio-attributed sources, (2) 25% from dedicated bio-based polymers, and (3) 45% from drop-in bio-based polymers. What would this require in terms of investment? Based on these assumptions, a 5% bio-based (including bio-attributed) polymer quota would generate €5.3 billion in investment, similar to the level of investment in first-generation biofuels. A subsequent 30% bio-based (including bio-attributed) polymer quota would generate €32 billion, similar to the level of investment in sustainable aviation fuels (SAF) in the next decades.

-

ZOOM-Interview with Alex Hogan (CEO of Vioneo) by Michael Carus (nova-Institut/RCI), 11 May 2026 (PDF)

Markets & Economy, Policy

3 Pages

38 Downloads 38 Downloads

2026-05

FREE

Free Shipping38

DownloadsThe vision of Vioneo as ‘fossil-free pioneers for the plastics industry, using green methanol to produce fossil-free polypropylene and polyethylene on a commercial scale‘ will be realised in China, not in Europe. Michael asks Alex why this is the case.

Mandatory EU legislation (quotas, definitions, regulatory differentiation) is the single most important enabler for Vioneo — and similar companies — to invest in Europe. Without it, the market remains voluntary, price-driven, and commercially unviable for premium fossil-free products.

As Europe is a more expensive production location than the US or Asia, the only way forward – as Alex Hogan makes clear – is to create clear, strong and lasting framework conditions in Europe to generate robust demand for renewable chemistry and plastics, as well as to build the infrastructure that makes production in the EU possible. These framework conditions are indeed being discussed and are planned, but it is not certain whether they will actually materialise, in what form, or when. But who invests in hopes and announcements?

-

CO2-based Fuels and Chemicals Conference 2026 (Proceedings, PDF)

Markets & Economy, Policy, Sustainability & Health, Technology

2026-05

150 € ex. tax

Plus 19% MwSt.Press

release Add to

cartThe proceedings of the CO2-based Fuels and Chemicals Conference 2026 (28-29 April 2026, https://co2-chemistry.eu) contain all released presentations (download of the program leaflet, PDF) and the press release of the three winners of the Innovation Award “Best CO2 Utilisation 2026″.

-

Support for bio-based feedstock in plastic packaging analysis under the Packaging and Packaging Waste Regulation (EU) 2025/40 (Affiliate product)

Markets & Economy, Policy, Sustainability & Health, Technology

100 Pages

2026-05

FREE

Free Shipping0

More

Downloads

infoNew publication from nova experts for the European Commission

This report assesses the role of bio-based feedstocks in plastic packaging under the EU’s Packaging and Packaging Waste Regulation (PPWR), with a focus on technological development and environmental performance. Although seventeen bio-based polymers are commercially available, they represent only ~1% of the global plastics market and account for just 4–5% of biogenic carbon in the EU chemical sector. Production capacity is concentrated in Asia (55%), followed by North America (17%) and the EU27+3 (14%). Despite their limited market share, there are no fundamental technical barriers to using them in packaging. Bio-based plastics offer a 30–70% reduction in greenhouse gas emissions compared to fossil-based alternatives, which supports the EU’s decarbonisation and circular economy goals. The report also evaluates the feasibility of setting targets for the use of bio-based materials, their equivalence with recycled materials and how sustainability criteria can be aligned with the Renewable Energy Directive (RED). Key recommendations include setting binding targets for bio-based content, establishing harmonised sustainability criteria, and adapting recycling infrastructure. Leveraging the complementarity of bio -based and recycled content could help to accelerate the EU’s transition to a climate-neutral packaging sector.Direct download via the renewable-carbon.eu/publications is not possible. -

AI Circular Economy Conference 2026 (Proceedings, PDF)

Markets & Economy, Policy, Sustainability & Health, Technology

2026-03

150 € ex. tax

Plus 19% MwSt.Press

release Add to

cartThe proceedings of the AI Circular Economy Conference 2026 (4-5 March, https://ai-circulareconomy.eu ) contain 25 conference presentations and the press release. Download of the program leaflet.

-

306 Downloads

2026-02

FREE

Free Shipping306

DownloadsBased on internal assessment of RCI member companies and joint analysis, this report reveals existing EU legislation which creates several roadblocks for the shift from fossil to renewable carbon, The report identifies ten concrete policy barriers across seven EU frameworks, including the ETS, REDIII, PPWR and SUPD.

Key findings show regulatory misalignment (creating non-level playing fields and regulatory uncertainty), outdated definitions and misleading classifications (excluding innovative, climate-friendly products from incentives and market access) and impractical administrative bureaucracy (often conflicting with industrial realities). The biggest barrier is not identified in a single regulation, but identified as the lack of coherent support for renewable carbon in the chemicals and derived materials economy.

The report provides practical suggestions to amend and fine-tune regulations in upcoming legislative revisions. It complements RCI’s policy proposal study published in 2025.

-

Biorefineries in Asia and the EU – an Explorative Study (PDF)

Markets & Economy, Policy, Technology

58 Pages

159 Downloads 159 Downloads

2026-01

FREE

Free Shipping159

DownloadsThe study aims to provide decision makers with a quick overview over the state of the bioeconomy in Europe and three selected countries in Asia, India, Thailand and Indonesia. Specific attention is placed on biorefineries, as they represent a key building block for the industry. Covered aspects include the political framework, technical pathways and existing infrastructure, alongside case studies. The study provides on-the ground insights from practioners in the field, includes a set of good-practice criteria to assess the prospects of biorefineries and offers a number of specific recommendations for future actions to expand the bioeconomy across continents.

-

179 Downloads

2026-01

FREE

Free Shipping179

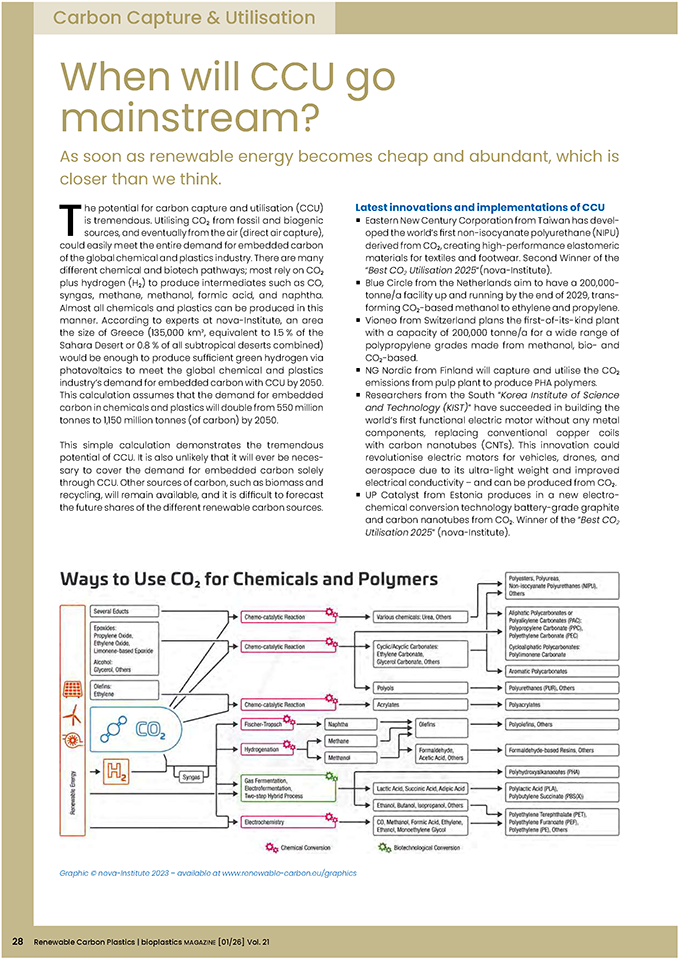

DownloadsAs soon as renewable energy becomes cheap and abundant, which is closer than we think.

The potential for carbon capture and utilisation (CCU) is tremendous. Utilising CO2 from fossil and biogenic sources, and eventually from the air (direct air capture), could easily meet the entire demand for embedded carbon of the global chemical and plastics industry. There are many different chemical and biotech pathways; most rely on CO2 plus hydrogen (H2) to produce intermediates such as CO, syngas, methane, methanol, formic acid, and naphtha.

Almost all chemicals and plastics can be produced in this manner. According to experts at nova-Institute, an area the size of Greece (135,000 km2, equivalent to 1.5 % of the Sahara Desert or 0.8 % of all subtropical deserts combined) would be enough to produce sufficient green hydrogen via photovoltaics to meet the global chemical and plastics industry’s demand for embedded carbon with CCU by 2050. This calculation assumes that the demand for embedded carbon in chemicals and plastics will double from 550 million tonnes to 1,150 million tonnes (of carbon) by 2050. This simple calculation demonstrates the tremendous potential of CCU.

-

Case Studies Based on Peer-reviewed Life Cycle Assessments: Carbon Footprints of Different Renewable Carbon-Based Chemicals and Materials (2nd, Extended Version) – RCI Report (PDF)

Sustainability & Health

67 Pages

867 Downloads 867 Downloads

2026-01

FREE

Free Shipping867

DownloadsThis report broadens the scope of the brochure “Case studies based on peer-reviewed Life Cycle Assessments – Carbon Footprints of Different Carbon-Based Chemicals and Materials”, published in November 2023. The initial brochure presented five peer-reviewed studies that drew strong interest from experts, policymakers, and industry leaders for their insights into the carbon footprints of various carbon-based chemicals and materials.

This second, extended version includes seven peer-reviewed LCAs from participating member companies: Braskem, Econic, Fibenol, LanzaTech, Lenzing (update), Peter Greven and Primient Covation.

These expanded contributions will deepen understanding of carbon footprints and further support RCI’s commitment to

data-driven sustainability.DOI No.: https://doi.org/10.52548/HRPM7087

-

Recycling Becomes Feedstock for Europe – Let’s Dare More Autonomy (PDF)

Policy

65 Pages

530 Downloads 530 Downloads

2026-01

FREE

Free Shipping530

DownloadsThe paper shows how this goal of transformation or defossilisation can be implemented step by step and how legal areas can be better integrated at EU level, which will result in new priorities for both sectors. For example, in waste management, much of what does not contribute to the carbon supply of the chemical industry can be phased out gradually. It also includes enabling all recycling technologies, from mechanical and physical to chemical processes and even incineration with CO₂ capture and utilisation, since all processes are needed in the transformation for the different waste fractions and target products. Overall, the ten proposals derived and analysed in the paper also lead to a significant reduction in bureaucracy.

There are some important proposals that build on instruments already introduced by the EU, such as substitution quotas for selected plastics sectors. The authors also specify proposals that are under discussion or being raised by Member States. However, there are also proposals to phase out existing regulations. It is important that the proposals build on each other and are implemented in a coordinated manner as part of a self-contained, phased overall package.

Fortunately, greater autonomy is becoming mainstream in the EU and is also one of the cornerstones of the new EU Council Presidency. However, unless it becomes practical, greater autonomy and resilience will remain nothing more than a narrative. And the path to achieving this will be fraught with difficulties.

DOI No.: https://doi.org/10.52548/LFPX3960

-

2025-12

FREE

Free Shipping2

More

Downloads

infoThe fashion industry is under growing pressure to shift towards more sustainable production methods and materials. Traditional petroleum-based materials dominate the textile and footwear industry. There is increasing interest in exploring alternative, more sustainable feedstocks, such as bio-based materials derived from carbon capture technologies. These alternatives offer potential environmental benefits but require thorough analysis to understand the technical feasibility, environmental impact, and regulatory considerations involved.

The nova-Institute (hereafter referred to as nova) was engaged by Fashion for Good and some of its partners to conduct an in-depth assessment of sustainable feedstocks and conversion technologies for producing polymers, specifically focusing on bio-(PET, PA, EVA and BDO). The aim was to create a comprehensive understanding of the technological routes available for using bio-based feedstocks and emerging CO2 conversion technologies in the production of polymers used in the textile industry. Additionally, nova assessed sustainability standards and certification schemes to ensure the feedstocks meet stringent environmental and social criteria.

Direct download via the renewable-carbon.eu/publications is not possible.

Please follow this link:

https://www.fashionforgood.com/case-study/biosynthetic-feedstock -

RCI Webinar: Success Stories RCI 2025 and Outlook to 2026 – Project Results and Position Papers (PDF)

Policy, Sustainability & Health

59 Pages

283 Downloads 283 Downloads

2025-12

FREE

Free Shipping283

DownloadsThe free RCI webinar on 9 December 2025 presented the RCI Success Stories 2025 and offered an Outlook to 2026. It showcased RCI’s policy impact at EU, national and international levels, highlighted key publications and scientific results (including the biomass study, Policy Proposals, LCA methodologies, sustainability criteria paper, and analysis of recent updates to methane and fossil CO2 emissions data in Life-Cycle Inventories (LCI)), and summarised member activities such as expert groups, roundtables, and survey insights. The webinar also introduced RCI’s ongoing and upcoming projects for 2026, including biodiversity, policy barriers, carbon flows, LCA case studies, and awareness-building initiatives.

-

Advanced Recycling Conference 2025 (Proceedings, PDF)

Markets & Economy, Policy, Sustainability & Health, Technology

2025-12

150 € ex. tax

Plus 19% MwSt.Press

release Add to

cartThe proceedings of the Advanced Recycling Conference 2025 (19-20 November, https://advanced-recycling.eu) contain 41 conference presentations, the conference journal, sponsor documents and the press release.

-

Renewable Materials Conference 2025 (Proceedings, PDF)

Markets & Economy, Policy, Sustainability & Health, Technology

2025-10

200 € ex. tax

Plus 19% MwSt.Press

release Add to

cartThe proceedings of the Renewable Materials Conference 2025 (22-24 September 2025, https://renewable-materials.eu) contain all released 68 presentations, the conference journal and the press release of the three winners of the Innovation Award “Renewable Material of the Year 2025″.

-

Increased Methane Emissions in Crude Oil and Natural Gas Supply: Implications for the Carbon Footprint of Petrochemicals – RCI Report (October 2025)

Sustainability & Health

39 Pages

636 Downloads 636 Downloads

2025-10

FREE

Free Shipping636

DownloadsThis scientific background report by RCI shows that recent updates to leading LCI databases (ecoinvent 3.9–3.11) reveal a major underestimation of methane emissions from oil and gas supply chains. Enhanced satellite data on flaring, venting, and leaks highlight large inconsistencies compared to sources such as IEA, IOGP, and the World Bank. For instance, IEA now reports oil-related methane emissions up to 15 times higher than IOGP, with extreme differences for Russia (10-fold) and Saudi Arabia (40-fold). These revisions sharply increase the carbon footprint of fossil feedstocks, with naphtha nearly tenfold higher and significant rises for ethylene, propylene, and ethylene glycol. As a consequence, plastics such as PE, PP, and PET show 20–30% higher footprints. By contrast, renewable carbon alternatives gain ground: bio-based plastics now appear 12–27% more climate-friendly, with even greater advantages when biogenic carbon uptake is included.

The RCI report urges policymakers to rapidly integrate methane regulation and updated LCI data into climate strategies. Key recommendations include regular database updates, expanded emissions tracking, harmonized reporting, and stronger support for renewable carbon solutions.

DOI: https://doi.org/10.52548/RQJN5517

-

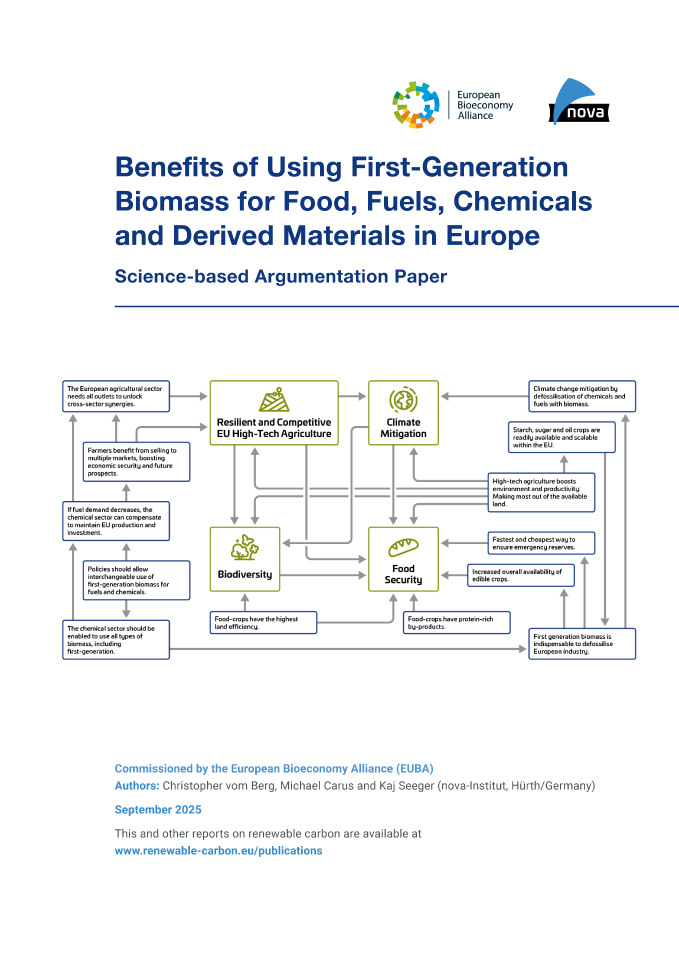

Benefits of Using First-Generation Biomass for Food, Fuels, Chemicals and Derived Materials in Europe (PDF)

Policy, Sustainability & Health

16 Pages

1188 Downloads 1188 Downloads

2025-09

FREE

Free Shipping1188

DownloadsKey messages – Benefits of using first-generation biomass for food, fuels, chemicals and derived materials

First-generation biomass in non-food applications increases food security.

Using first-generation biomass for non-food applications strengthens food security by increasing overall availability of feedstock and market stability. At the same time, it also delivers valuable protein-rich by-products addressing the most critical needs for human and animal nutrition. The ability to shift crops between the food, feed, and industrial markets enables the EU and market players to respond swiftly to changes in demand and mitigate the risks associated with supply chain disruptions. Most importantly, using first-generation biomass for non-food applications offers a fast and economical way to set up and ensure an emergency food reserve.- First-generation biomass in non-food applications enhances a resilient and competitive EU agriculture

- First-generation biomass in non-food applications supports climate change mitigation

- First-generation biomass in non-food applications supports biodiversity protection

- High-tech agriculture further enhances the benefits of first-generation biomass.

DOI No.: https://doi.org/10.52548/GCJC4981