AI Circular Economy Conference 2026 (Proceedings, PDF) [Digital]

AI Circular Economy Conference 2026 (Proceedings, PDF) [Digital] Showing 41–60 of 428

-

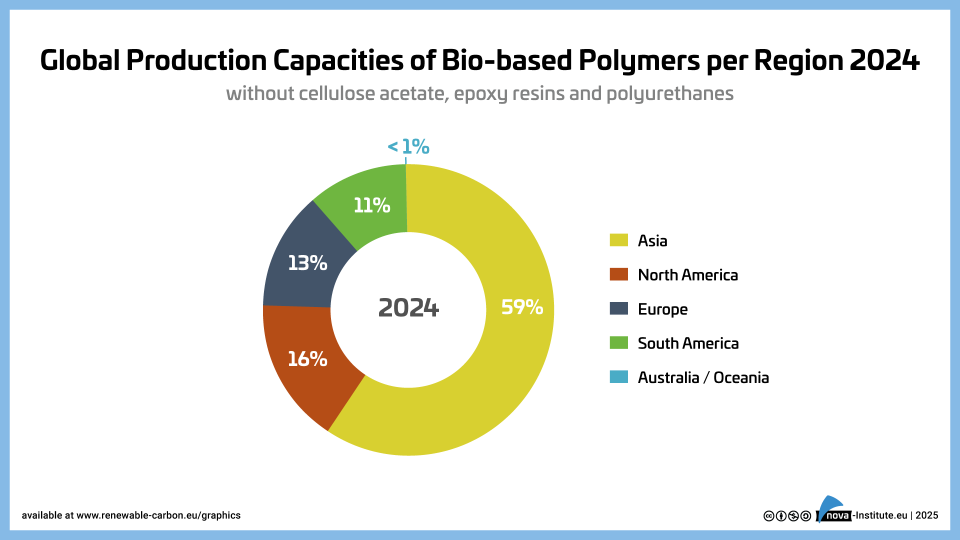

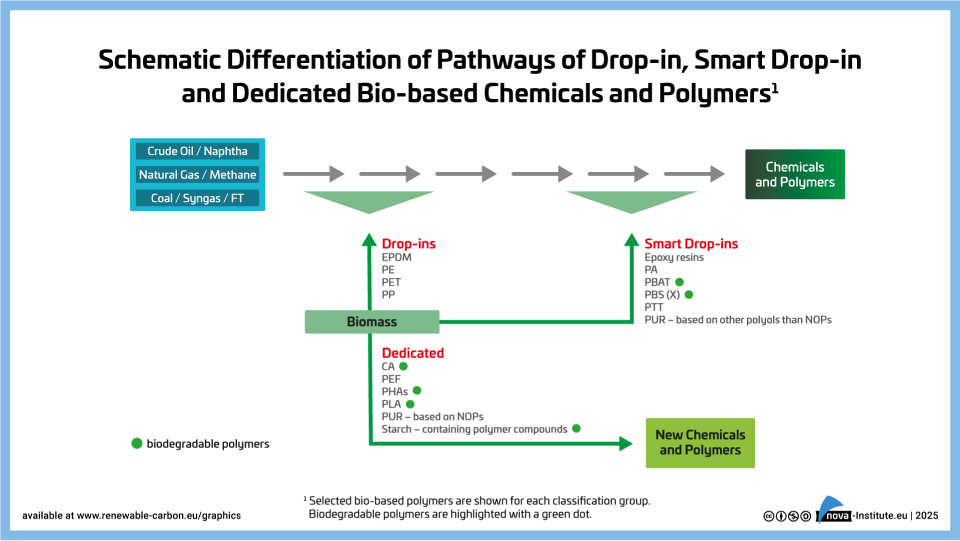

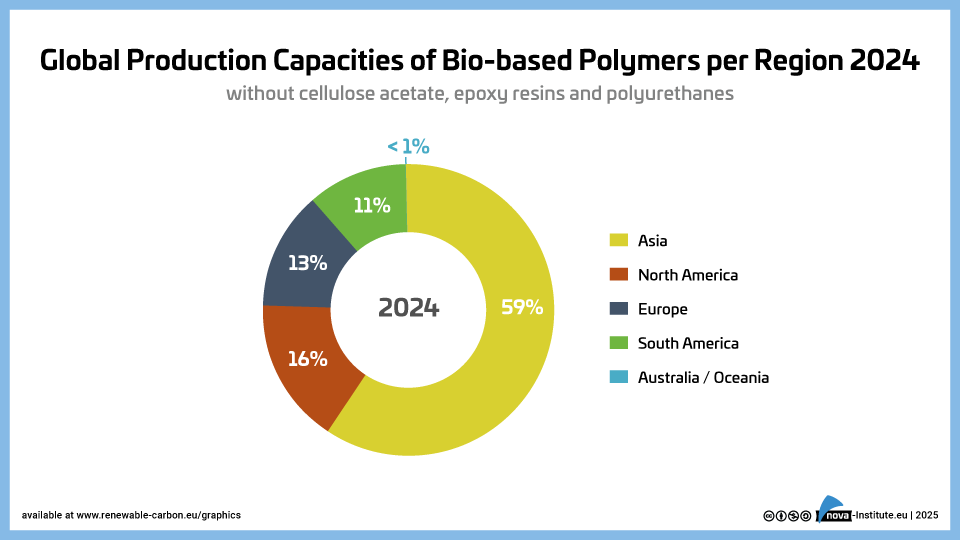

Global Production Capacities of Bio-based Polymers per region 2024 (PNG)

Markets & Economy

1 Page

83 Downloads

-

-

-

-

-

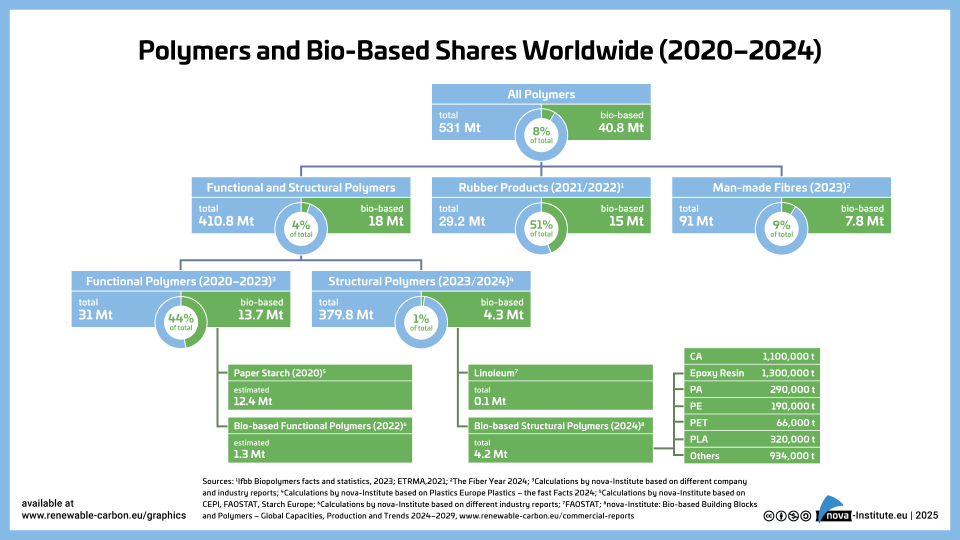

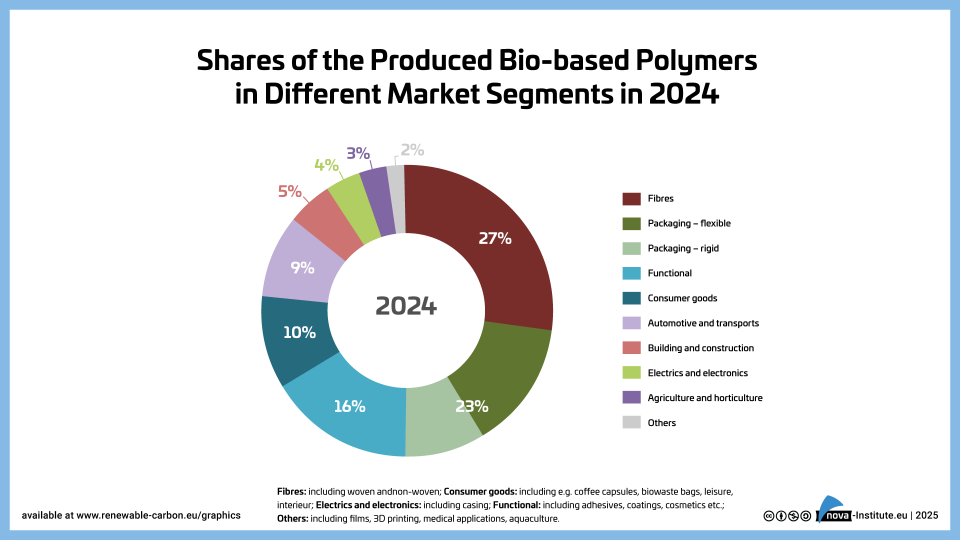

Shares of the Produced Bio-based Polymers in Different Market Segments in 2024 (PNG)

Markets & Economy

1 Page

135 Downloads -

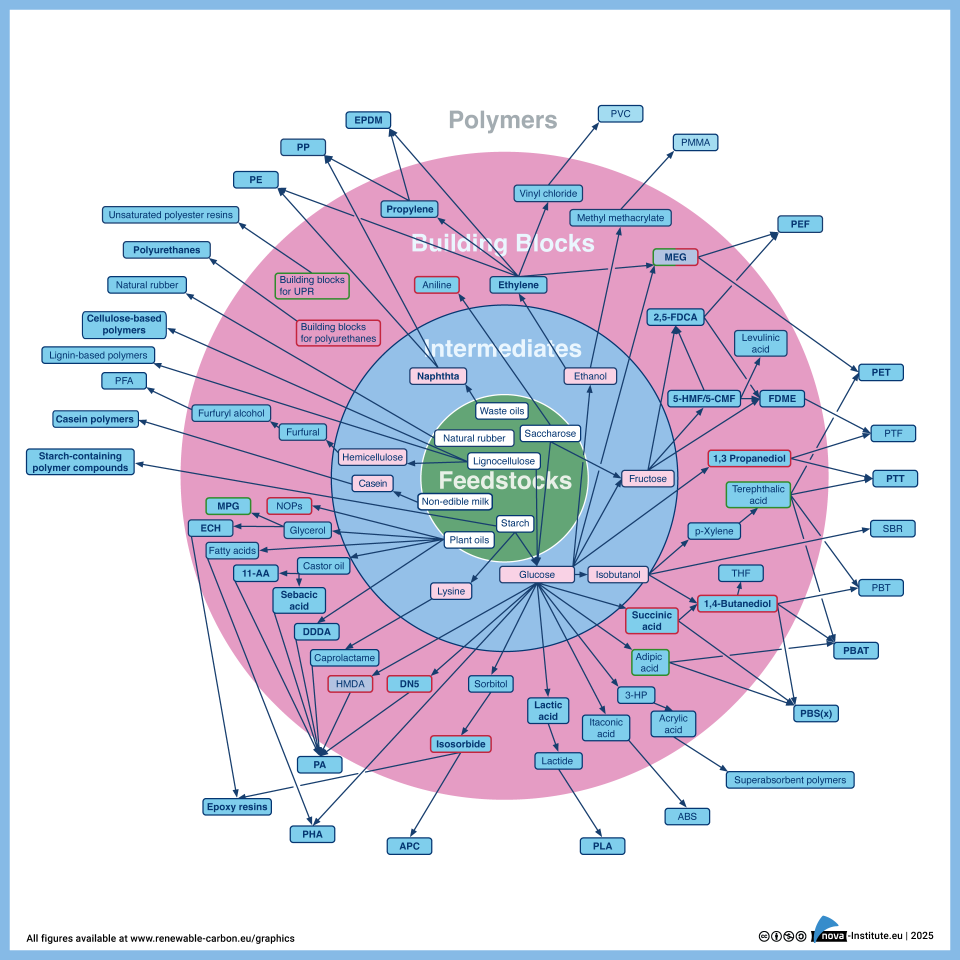

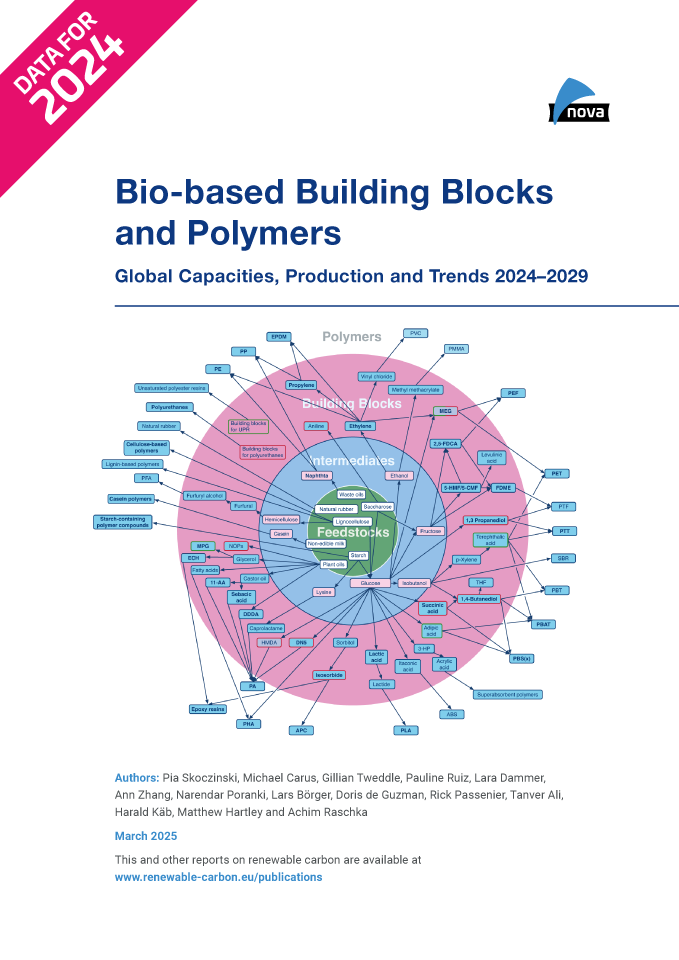

Bio-based Building Blocks and Polymers – Global Capacities, Production and Trends 2024–2029 (PDF)

NewMarkets & Economy

434 Pages

-

Evaluating LCA Approaches and Methodologies for Renewable Carbon Sources Report 1 of 3: Renewable Carbon in LCA Guidelines – RCI Report (March 2025)

Markets & Economy, Policy, Sustainability & Health

145 Pages

1150 Downloads -

Evaluating LCA Approaches and Methodologies for Renewable Carbon Sources Report 2 of 3: Renewable Carbon in Recycling Situations – RCI Report (March 2025)

Markets & Economy, Policy, Sustainability & Health

37 Pages

823 Downloads -

Evaluating LCA Approaches and Methodologies for Renewable Carbon Sources Report 3 of 3: Non-technical Summary – RCI Report (March 2025)

Markets & Economy, Policy, Sustainability & Health

15 Pages

1019 Downloads -

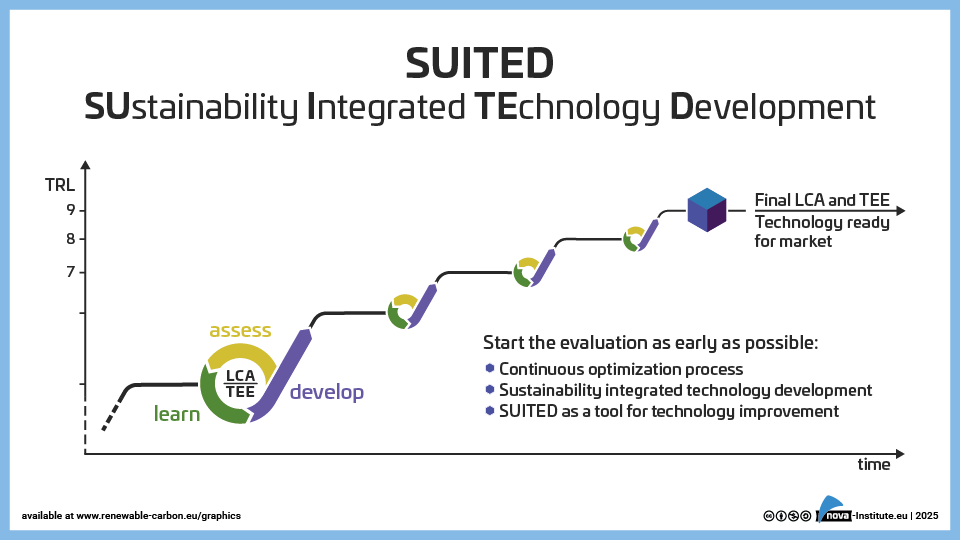

SUITED approach: SUstainable Integrated TEchnology Development (PNG)

Markets & Economy, Sustainability & Health

1 Page

27 Downloads -

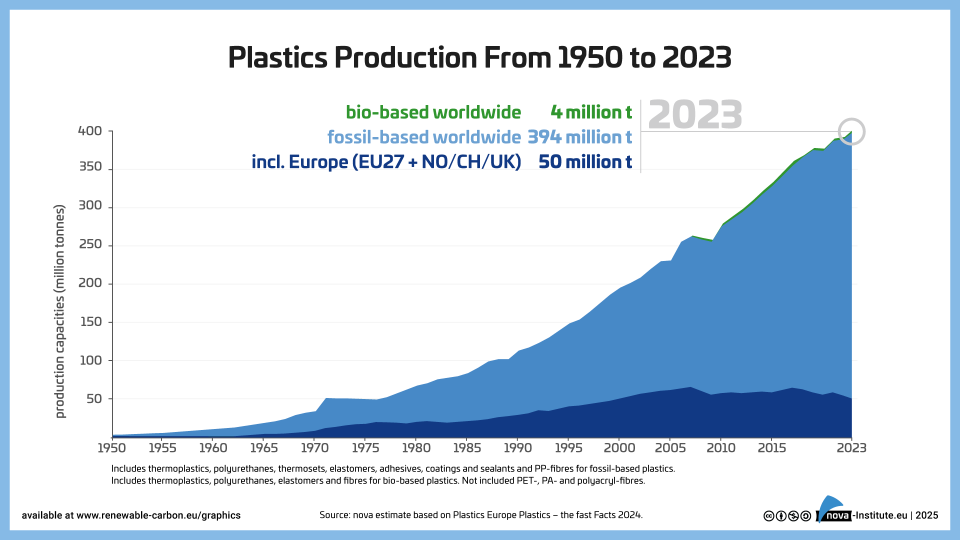

Bio-based Polymers Worldwide (PDF)

Markets & Economy, Policy, Sustainability & Health

5 Pages

868 Downloads -

Sustainable textiles – the way forward (PDF)

Markets & Economy, Sustainability & Health

6 Pages

603 Downloads -

Global Major Fibre Types by Production in % (PNG)

Markets & Economy, Sustainability & Health

1 Page

48 Downloads -

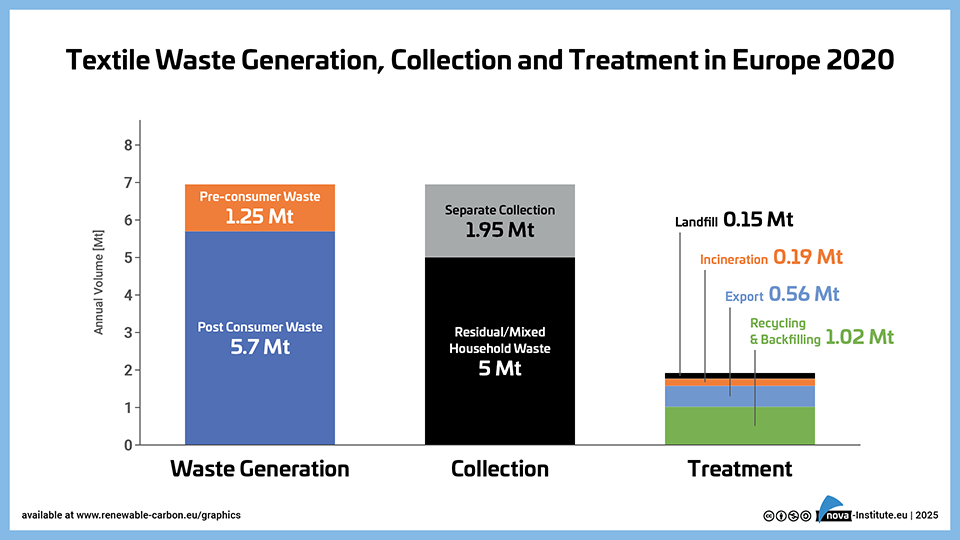

Textile-Waste-Generation-Collection-and-Treatment-in-Europe-2020 (PNG)

Markets & Economy, Sustainability & Health

1 Page

52 Downloads -

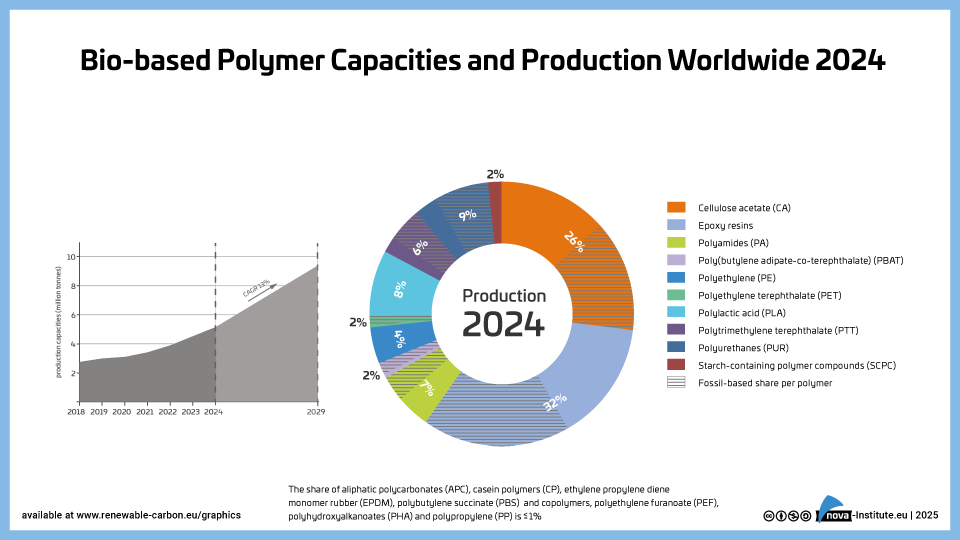

Bio-based-Polymer-Production-and-Bio-based-shares-2024 (PNG)

Markets & Economy, Policy, Sustainability & Health

1 Page

185 Downloads -

Global-Production-Capacities-of-Bio-based-Polymers-per-Region-2024 (PNG)

Markets & Economy, Policy, Sustainability & Health

1 Page

44 Downloads -

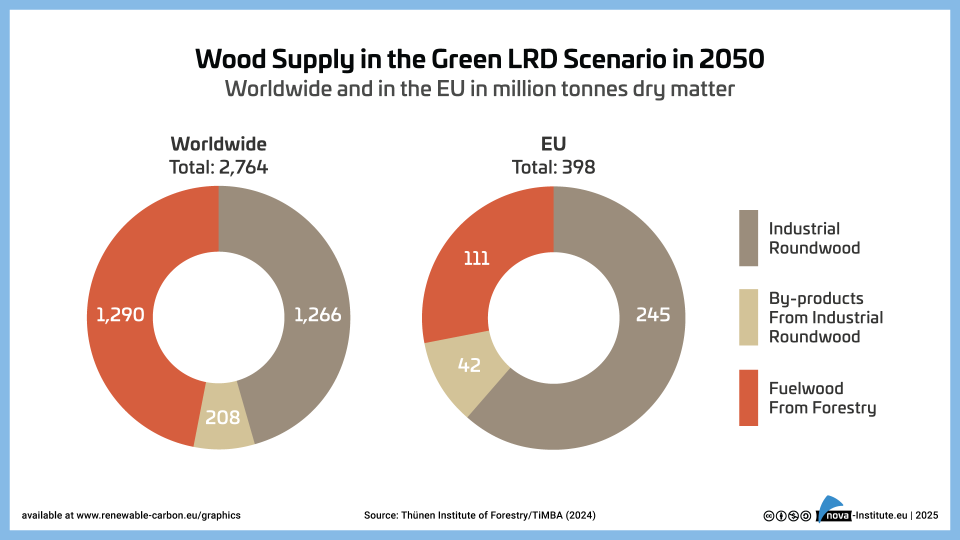

Wood Supply in the Green LRD Scenario in 2050 – Graphic (PNG)

Markets & Economy, Policy, Sustainability & Health

1 Page

14 Downloads -

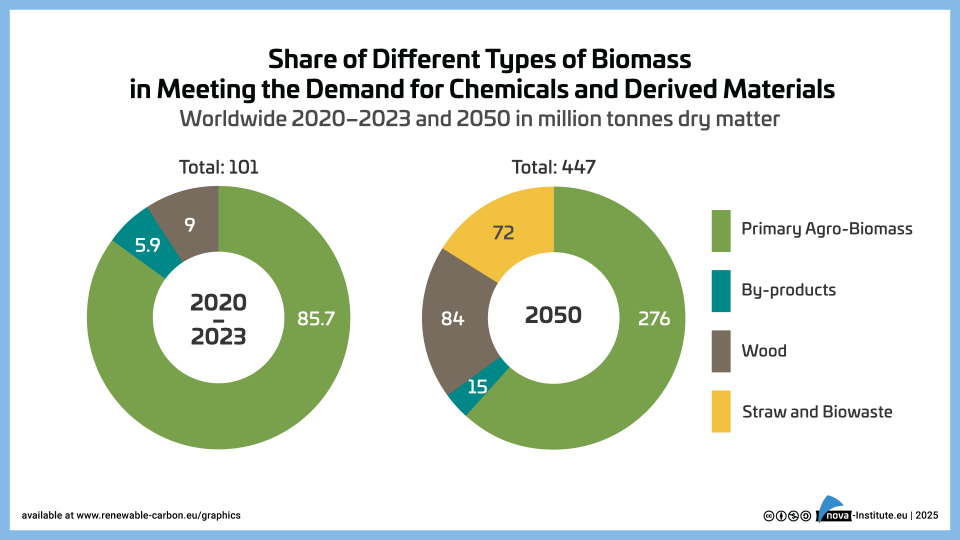

Share of Different Types of Biomass Worldwide 2023-2050 – Graphic (PNG)

Markets & Economy, Policy, Sustainability & Health

1 Page

67 Downloads -

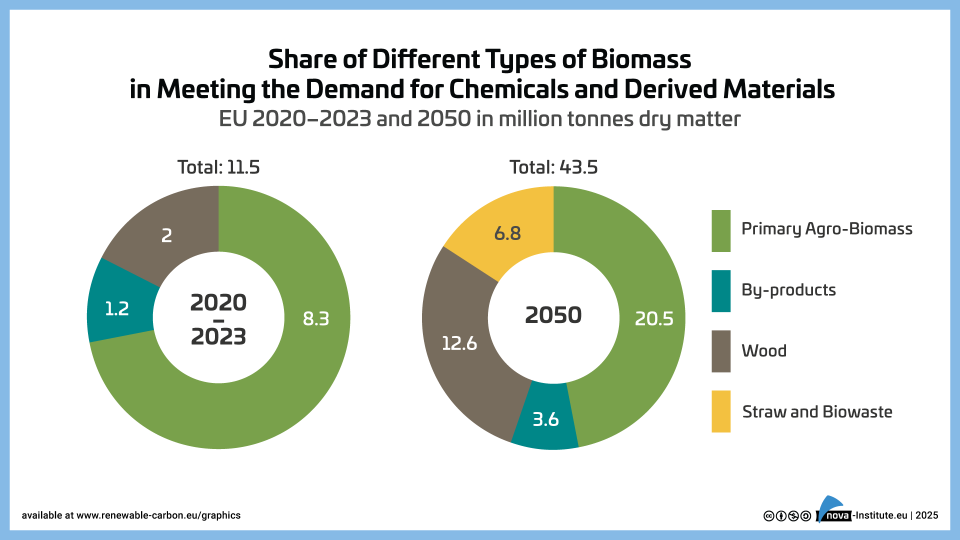

Share-of-Different-Types-of-Biomass-EU-2023–2050 – Graphic (PNG)

Markets & Economy, Policy, Sustainability & Health

1 Page

34 Downloads