Bioplastic materials are defined as materials that are either biodegradable and compostable; and derived from both renewable and non-renewable sources, or materials that are non-biodegradable and derived from renewable resources. As per a report by Pira International, from 2010, bioplastic technology is expected to change with the commercialisation of bioplastics produced directly by natural/genetically modified (GM) organisms and the introduction of non-biodegradable, bio-derived polyethylene (PE).

Bioplastic materials are defined as materials that are either biodegradable and compostable; and derived from both renewable and non-renewable sources, or materials that are non-biodegradable and derived from renewable resources. As per a report by Pira International, from 2010, bioplastic technology is expected to change with the commercialisation of bioplastics produced directly by natural/genetically modified (GM) organisms and the introduction of non-biodegradable, bio-derived polyethylene (PE).

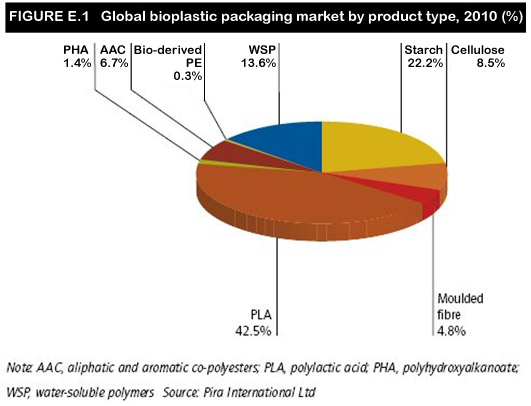

Pira expects these materials will account for a quarter of total bioplastic packaging market demand by 2020. Polyhydroxyalkanoates (PHA) are forecast to achieve a CAGR of 41% and bio-derived PE a staggering 83% over the period. Traditional bioplastic packaging technologies based on starch, cellulose and polyester are each forecast to show a decline in market share to 2020.

Bioplastic packaging is a highly concentrated market with the top five suppliers currently accounting for over 50% of bioplastic packaging market demand. Pira predicts major changes among the leading ranks of bioplastic packaging suppliers over the next 5-10 years.

Large petrochemical companies including Braskem, Dow Chemicals and Solvay are scheduled to commence bio-derived PE production by 2012 at industrial-scale facilities in Brazil. These companies are expected to be propelled into the top rank of bioplastic producers over the next five years. Telles, the joint venture PHA producer, is also expected to become a major world player. Several Chinese companies are known to be investing in significant capacity expansion programs that should propel them into leading market positions. US bioplastics producer Cereplast is planning to launch a range of all-natural algae-based resins by the end of 2010.

Also, several companies are exploring the development of bioplastics using carbon dioxide as a raw material. The potential for a process that converts waste carbon dioxide into a useful product is huge, but whether the material produced using this technique will prove commercially viable will ultimately depend on whether these new polymers are cost effective to produce.

A new sugar-based bioplastic that can be sourced from non-food crops and produced via a low energy process is also tipped to reach the market within the next five years. Rigid packaging has a projected share of 52% of the bioplastic packaging market in 2010 according to Pira, with flexible packaging accounting for the remaining 48%.

Retail and foodservice trays and containers are the largest single pack type for bioplastic packaging, followed by flexible film. Pira expects flexible packaging to take a growing share of the bioplastic packaging market over the next five to ten years. Adam Page, Head of Information at Pira, explains: “Demand will be driven by the commercialisation of bio-derived PE and PHA, and the wider availability and improved properties for biaxial oriented PLA (BOPLA) film.”

Europe is the largest regional market for bioplastic packaging with over half of world tonnage in 2010. It benefits from favourable consumer and retail attitudes to sustainable packaging, supportive government policies towards packaging waste recycling and a well-developed composting infrastructure.

Whilst North America currently trails Europe in terms of bioplastic packaging consumption, government and consumer attitudes are changing. Pira expects North America and Asia to show higher growth rates than Europe for bioplastic packaging over the forecast period.

Japan accounts for the lion’s share of Asian bioplastic packaging, mostly as a result of favourable government initiatives supporting bioplastic market development. Global demand for bioplastic packaging is forecast to reach 884,000 tons by 2020. This translates to a compound annual growth rate of 24.9% from 2010-15 slowing to a CAGR of 18.3% in the 5 years to 2020. According to the study, a new breed of bioplastics will be major drivers as packaging market demand gradually shifts from biodegradable and compostable polymers towards biopackaging based on renewable and sustainable materials.

The global market for Biodegradable Polymers is forecast to reach 1845 million lbs by the year 2015, as per a report by Global Industry Analysts. Principal factors driving growth include fast depletion of traditional sources of fossil fuel leading to the shift towards renewable sources, backlash arising out of rising environmental pollution, increased need to inhibit greenhouse gas emission, escalating costs of petroleum feedstock and wide scale availability of naturally occurring cheap feedstock, and increasing preference for environmental friendly products.

Massive volumes of plastic products are disposed worldwide every year, exerting enormous pressure on the ecological balance. All such plastics form potential candidates for substitution by biodegradable polymers in future. Applications of biodegradable polymers, which were hitherto mostly confined to compostable waste bags/carrier bags, agriculture mulching film, and catering sectors, is rapidly widening to other sectors, including automotive, electronics, toy making, and healthcare.

With enhanced process ability, extending customer base and improved costs, biodegradable polymers are proving to be environmentally beneficial and economically viable alternative to conventional polymers. These polymers have generated wide scale interest amongst customers and companies alike. The presence of a sizable potential market has opened up a plethora of opportunities for companies within the chemical, agricultural, and plastic sectors.

Europe presently accounts for majority of the biodegradable polymers market, as stated in the report. However, the soaring landfill prices in the US provide the market with significant growth opportunity. Factors such as fast depletion of petroleum-based raw materials, growing consumer awareness, global warming and increasing concerns over solid waste disposal, would continue to drive demand for biodegradable polymers in the US. In addition, Asian countries, including China and Japan, also exhibit strong growth potential for biodegradable polymers. Growing demand for eco-friendly products, mounting production volume, and the plastic waste control regulation promises a sanguine future for biodegradable polymers in China.

Packaging (Loose-fill/Other), which traditionally represented the largest application area for biodegradable polymers, has been losing ground to other emerging applications, such as compost bags, agriculture and horticulture. Lack of municipal composting facilities, curbside collection, popularity of air filled plastics as well as other materials for packaging protection is limiting the growth of biodegradable polymers in loose-fill packaging applications. This is in turn presenting lucrative opportunities for growth of biodegradable polymers in other major applications such as compost bags. The global market for biodegradable polymers from compost bags application is forecast to grow at a CAGR of 20.9% over the analysis period.

Polylactic acid biopolymers and Copolyester-based biopolymers are the most widely used biodegradable polymers used. In addition, there is a continued demand for starch biopolymers in modified form, or blends (starch blended with other polymer or polyolefin).

Major suppliers of starch-based biopolymers include Novamont, DuPont, among others. Major players of biodegradable polymers profiled in the report include Durect Corp., American Excelsior Company, BioGroupUSA Inc., BASF SE, BIOTEC GmbH & Co. KG, Cereplast Inc., Cortec Corp, E. I. du Pont de Nemours and Company, Daicel Chemical Industries Ltd., Eastman Chemical Company, ECM BioFilms Inc., FP International, IRe Chemicals Limited, Metabolix Inc., Mitsubishi Plastics Inc., Mitsui Chemicals Inc., National Starch and Chemical Company, NatureWorks LLC, Novamont S.p.A, Perstorp UK Limited, Rodenburg Biopolymers B.V., ReNewable Products Inc., Showa High Polymer Co. Ltd., Storopack Hans Reichenecker GmbH, Toyobo Co. Ltd., among others.

Source

plastemart.com, 2011-01-14.

Supplier

American Excelsior Company

BASF SE

BioGroupUSA Inc.

BIOTEC GmbH & Co. KG

Braskem

Cereplast Inc.

Cortec Corporation

Daicel Chemical Industries Ltd.

DuPont

Durect Corp.

Eastman Chemical Company

ECM BioFilms, Inc.

FP International

IRe Chemicals Limited

Metabolix

Mitsubishi Plastics, Inc.

Mitsui Chemicals

National Starch and Chemical Company (USA)

NatureWorks LLC

Novamont S.p.A.

Perstorp

PIRA International

ReNewable Products Inc.

Rodenburg Biopolymers B.V.

Showa High Polymer Co. Ltd. (Shanghai)

Storopack

Toyobo Co. Ltd.

Share

Renewable Carbon News – Daily Newsletter

Subscribe to our daily email newsletter – the world's leading newsletter on renewable materials and chemicals