Download policy paper, graphics and market pull list at www.bio-based.eu/policy

The European Union will need a new political framework for rolling out its bio-based economy by 2020 at the latest. The existing framework does not create sufficient market pull for implementing innovative, bio-based technologies. The best framework would allow for the highest resource efficiency, the most innovation capacity, the highest value added, the most employment and the greatest protection of ecosystems. The current framework creates a non-level playing field between bio-based materials and energy, triggers never-ending discussions about a variety of issues such as land-use change and multiple counting of different biomass sources in quotas, and ultimately hinders Europe’s bio-based economy from tapping into its full potential of innovation, investment and jobs. There are several ways to change this framework. With this position paper, nova-Institute’s policy experts contribute to the current debate by assessing and evaluating different options for framework reform.

Authors: Michael Carus, Lara Dammer and Roland Essel (nova-Institute)

The bioenergy and biofuels sector finds itself in troubled waters; many member states of the EU are not on track to meet the targets set out in the “Renewable Energy Directive (RED)” and investments are stagnating. Political and public debates focus more on the effects on global food prices, pressure on ecosystems, and direct as well as indirect land-use change, rather than previous growth and future opportunities and investments. This is partly due to the fact that the whole sector (with some exceptions in the wood heating market) is strongly dependent on incentives. If those are reduced, many companies might face bankruptcy and new investments will stop – as can already be witnessed in many member states.

The material use of biomass presents an alternative to energy use. It can create much more added value per tonnes of biomass, innovation, employment and investment and – if done right – can contribute to the economically and ecologically viable future of the European Union. The current framework, however, focuses only on the energy sector in terms of market instruments; bio-based materials and chemicals are only considered in research policies without any widespread application of novel bio-based materials so far.

This is also confirmed by the “Organisation for Economic Co-operation and Development” (OECD 2013): “Generally, biofuels policy support is much greater than it is for either bio-based plastics or bio-based chemicals. This is likely to make the development of the bioeconomy uneven, and may disfavour the use of biomass for bioplastics and bio-based chemicals. It may also constrain the development and operation of integrated biorefineries.”

It is Time for a Change and a New Start

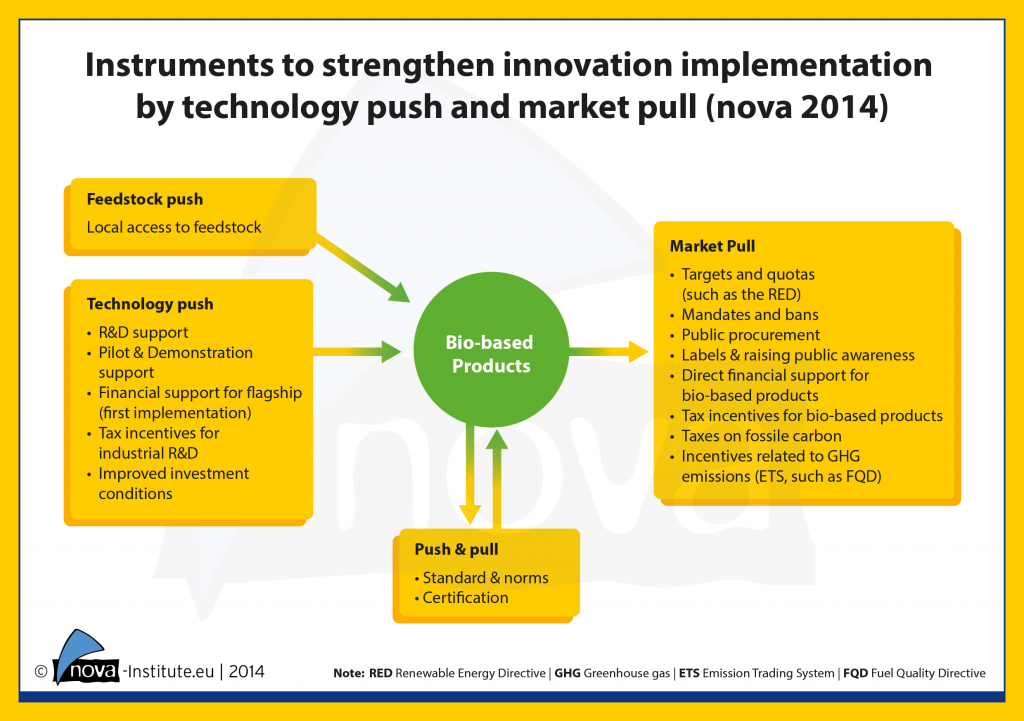

The number of ways to reform of the existing political framework is limited: the main instruments are shown in the figure below, which follows Joseph Schumpeter’s theories of technology push and market pull factors. A technology push implies that a new invention is pushed onto the market through research and development (R&D), production and sales functions without proper consideration of whether or not it satisfies a user need. In contrast, an innovation based upon market pull has been developed by the R&D function in response to an identified market need. (Martin 1994)

With this position paper, nova-Institute’s policy experts contribute to the current debate by assessing and evaluating different options for framework reform.

Feedstock Push

From the “push” perspective, most assessments come to the same conclusions about what needs to be done. A bio-based economy can only flourish when local access to feedstock at a reasonable price can be guaranteed – otherwise all investment will be limited to a few harbours, where biomass can be imported from other countries.

Biomass is not rare in the EU, but allocating it properly has its issues. Mainly because of the existing incentives of the Renewable Energy Directive, a number of biomass sources are only accessible for bioenergy and biofuels, but not for bio-based chemicals and materials. This can be addressed by changing the market pull mechanisms.

The reforms of the Common Agricultural Policy (CAP) will result in a change of biomass supply in the future. “In 2017, after the abandonment of sugar quota, we will have lots of cheap sugar in Europe. Europe is the most efficient producer of sugar in the world, in Northern France, Flanders, and Southwest Holland. Sugar, a first generation feedstock, is one of the most sustainable resources, easily and cheaply fermentable” (Carrez 2014). It will therefore be of crucial importance that the bio-based chemical and material industries have access to European sugar. The latest analyses also question the preference of lignocellulosic feedstock in general (Carus & Dammer 2013).

Another important aspect is the mobilisation of wood resources in Europe, where forests show more growth than extraction, with especially small private forests systematically being underutilized.

Technology Push

Concerning technology push, the European Union has always been competitive and has at times been at the forefront of research and development. The new programmes, such as Horizon 2020, develop the R&D framework further and also address more market and business oriented factors. This seems like a suitable way to help newly developed processes and products achieve market success.

The support of pilot- and demonstration plans as well as the financial support of flagship investments (all weak points in the past) are covered by the new cooperation between the European Commission and the Bio-based Industries Consortium (BIC): The Bio-Based Industries Joint Undertaking launched its first Call for Proposals in summer 2014 (http://biconsortium.eu/call-2014). 3.7 billion € will be made available to realise the potential of bio-based industries in Europe.

In the future, the range of R&D activities should be carefully chosen and should not be limited to the conversion of lignocellulosic feedstocks, waste biomass and algae; research should also be done into the use of sugar beet in the chemical and plastic industry, the use of rapeseed oil in the oleochemistry, and biomethane for the production of chemicals and polymers. Moreover, the huge demand for cellulose fibre in textiles should not be ignored; it could be a great opportunity for the European pulp industry. Finally, the investment climate in Europe is weak compared with many locations in America and Asia. The bio-based economy suffers from this due to general issues, as well as the existing market pull mechanisms in the bioenergy and biofuel sectors, which create market distortion, artificial shortage and higher feedstock prices.

What can Europe learn from other regions in the world? Tax incentives for industrial R&D could be helpful to strengthen market oriented research and development outside the official EU and member states’ programmes.

Push & Pull

Standards and certification can be understood as both push or pull instruments. DG Enterprise and Industry with its “Commission Expert Group for Bio-based Products” focuses on standards and certification, as well as on market pull measures such as labelling, public awareness and public procurement for bio-based products.

Triggered by the DG Enterprise and Industry, the European Committee for Standardization (CEN) made substantial progress over the last years. A dedicated technical committee (TC 411) deals with “Bio-based products” and in August 2014 the European Standard EN 16575 on “Bio-based products – Vocabulary” came into force. This standard defines a bio-based as a product which is “wholly or partly derived from biomass. … The bio-based product is normally characterised by the bio-based carbon content or the bio-based content. For the determination and declaration of the bio-based content and the bio-based carbon content, see the relevant standards of CEN/TC 411.” The certification of “sustainable feedstock” is also on the right track: established systems such as ISCC, RSB or FSC and PEFC can be used wherever it is appropriate.

All above-mentioned activities are important for establishing a long-term market of bio-based chemicals, materials and products. However they barely help in the everyday competition for biomass and market access, and are relatively weak instruments which are not enough to trigger large-scale effects and investment.

A strong instrument would be to make bio-based materials and products economically attractive or even mandatory for the industry or end consumers; as an example, this was successfully accomplished for bioenergy, biofuels, and solar and wind energy.

Market Pull

nova-Institute discusses the following as strong market pull instruments: targets and quotas; mandates and bans; direct financial support; tax incentives; and the EU Emissions Trading System (ETS). All possible options will be described briefly and evaluated below. Furthermore, we will also discuss the “no incentives at all” option.

Targets and Quotas

Today’s most important market pull instrument in the bio-based sector is the Renewable Energy Directive (RED), which creates artificial demand for bioenergy and biofuels. In terms of investment and market volume, this has been very successful. However, several problems of the current framework have started to become apparent over the last few years: there is for example the fact that many member states are not on track with meeting their quotas; endless discussions on LUC and iLUC; certification of sustainable feedstocks; the system of multiple counting for certain feedstocks; their classifications as waste, residue or co-product; and that feedstock bottlenecks have appeared due to the increased and unbalanced demand for biomass. Moreover, the existing RED framework does not take resource efficiency, cascading use and circular economy into account.

At the same time, the “true” bio-based economy is not picking up any speed. This is caused, among other things, by the framework conditions created by the RED, which systematically prevent new developments and investments in higher value added applications, such as bio-based chemicals and materials, by only supporting energy use of biomass.

Several member states question the planned increase of the renewable energy quota by 2030 (from 20% to 40%, baseline 1990) and would prefer to avoid technological obligations. The current mood in many member states and also the EU Commission seems to favour the option to not continue the existing RED framework after 2020. Directing the market by “targets and quotas” is more questionable than ever, and if this strong instrument is to survive after 2020, it will have to be substantially modified.

Earlier this year, nova-Institute published the “Proposals for a Reform of the Renewable Energy Directive to a Renewable Energy and Materials Directive (REMD) – Going to the next level: Integration of bio-based chemicals and materials in the incentive scheme” (Carus et al. 2014a). The reform proposal is aimed at creating a level playing field for bio-based chemicals and materials with bioenergy and biofuels in Europe, which would allow for the most value added and the highest reductions of greenhouse gas (GHG) emissions with a limited amount of biomass while preserving and expanding the existing infrastructures of bioenergy and biofuels.

Advantages of a RED reform – keeping targets and quotas

- No sudden ending of subsidies, but a continuous development of the bio-based economy, including bio-based chemicals and materials;

- Possibility to fulfil the existing CO2 reduction targets and even to increase binding targets beyond 2020 as planned, because it would be possible to fulfil them in more ways than today.

Disadvantages of a RED reform – keeping targets and quotas

- Complicated implementation of detailed instructions and further difficulties in avoiding unwanted market distortions in the future;

- Long-term higher energy and fuel costs for consumers, possibly also for bio-based products.

Mandates and Bans

Mandates and bans can successfully exert targeted influence on markets. A recent example is the ban on the highly inefficient light bulbs, which has significantly contributed to accelerating the light emitting diode (LED) revolution. Today, there are LEDs for almost any light application, with strongly increased efficiency and lower market prices.

There are similar opportunities for bio-based products that offer considerable ecological and health advantages for many applications. So far, however, most of these opportunities have been left unused, with the exception of the planned ban on single-use plastic bags being discussed in the EU.

The reasons for mandates and bans should always be based in environmental and health protection, not in the property of being “bio-based”. Together with several experts, nova-Institute has compiled a three-page list with specific suggestions for mandates and bans and put it forward for discussion (www.bio-based.eu/policy). It is fascinating to see how many of the proposed measures would make sense in terms of environmental and health policy and which application ranges would be covered by them.

This approach could also (finally) rouse some interest for the bio-based economy and bio-based products in the Environmental Ministries of the member states. With a view on bioenergy and biofuels, some officials have always been sceptical, but if bio-based chemicals and materials offer true environmental advantages, the Ministries of the Environment should become more active in the discussions and the processes of the bio-based economy.

The example of plastic microparticles serves to illustrate this point: they can be found in many cosmetics and body care products and leak uncontrollably into the environment, where they pollute, for example, marine environments and are found in many marine animals. Microparticles from bio-based polymers, which degrade completely in marine water (as for example PHA/PHB), would be a good solution for this problem. Why should their usage not be made mandatory? Several other examples can be found on the list (www.bio-based.eu/policy).

Advantages of mandates and bans

- Environmental and health reasons can be powerful political tools and can find much support from policymakers, society and NGOs;

- Properly designed mandates and bans can create considerable market incentives, prompt innovations and encourage investment in Europe.

Disadvantages of mandates and bans

- Mandates and bans constitute strong market interventions which are often rejected and opposed by established industries;

- Political steadfastness will be necessary in order to enforce comprehensive mandates and bans.

Public Procurement

European public authorities spend almost 2,000 billion € on goods and services every year. This means that public procurement can be a tool for creating market pull, also for innovative bio-based products. The BioPreferred® program of the USDA is a very pragmatic example of how public authorities can promote bio-based products. In Europe, there is no such thing and public procurement is not yet used as a market pull instrument for bio-based products. Two existing procurement tools could principally cover bio-based products, too, but presently do not: Green Public Procurement (GPP) and Public Procurement of Innovation (PPI). However, slowly but surely, things are being set in motion to change the current situation.

On the European level, public procurement is covered in a working group of the “Commission Expert Group for Bio-based Products” and also in a Horizon 2020 call that aims to build procurement networks for innovative bio-based products. There are already a multitude of national and regional platforms that support sustainable procurement, and some of them also contain dedicated information on bio-based products. The FP7 project Open-Bio has collected these product information platforms recently (www.open-bio.eu).

As mentioned above (“Push & Pull”), however, we think that public procurement, albeit an important contributing factor for market establishment of bio-based products, will only have a limited impact on the markets.

Labelling and Raising Public Awareness

Labels offer targeted information about the advantages of the labelled products in order to support buying decisions of consumers. It is currently being discussed to support the market pull of bio-based products with a label informing consumers about their bio-based content. Several methodological challenges have to be faced in order to avoid false claims (“greenwashing”) or simple misunderstandings. Discussions are on-going in the “Commission Expert Group for Bio-based Products” and in the research project Open-Bio, mostly with a focus on the EU Ecolabel (www.open-bio.eu). Similarly to public procurement, we think that labels could play a role in the market establishment of bio-based products, but will not be enough to help in the everyday competition for feedstock and investments.

Direct Financial Support

Another possibility is to give direct financial support for the feedstocks of certain bio-based product lines; however this somewhat successful refund system was discontinued entirely years ago. The financial support of production and marketing of bio-based products is generally also seen as critical and is difficult to harmonize with competition law. Furthermore, it would require providing considerable direct financial means. With the exception of targeted and temporary market introduction programmes, direct financial support is therefore not considered as a relevant tool for the future design of the framework.

Tax Incentives

Today, the worldwide chemical industry pays no taxes on the use of crude oil or natural gas as feedstock. A tax on fossil carbon used by the chemical industry would be a strong instrument to make biomass sources attractive. However, this approach can only be implemented on a global level, since considerable market distortion would otherwise result, with negative effects for Europe.

Different kinds of tax incentives for bio-based products are possible in the member states and have been investigated in different reports. In some member states this instrument was already used, for example for packaging materials (Belgium, The Netherlands). Brussels could enable the member states to use tax incentives, with the responsibility for implementation falling on the member states. The current discussion about the applicability of reduced VAT for environmentally advantageous products is leaning that way.

Incentives / Regulations Related to GHG Emissions

Expanding the whole Emission Trading System (ETS) in order to cover the material use of industrial production and not just the energy use is conceivable in principle, since an improved choice of materials can also reduce greenhouse gas emissions by substantial amounts. First steps in this direction are being made internationally for the wood sector in order to account for stored GHG in wood-based products. This presents quite a methodological challenge. Also, the certificates would have to be made much more expensive in order to gain real effects. Another option would be imposing obligatory GHG reduction goals for specific economic sectors, such as for example the plastics industry. The targets could be reached through increased use of recycled materials, petro-chemical plastics with a lower carbon footprint or bio-based plastics.

No Incentives At All

Another option which is currently under serious discussion and which has quite a bit of charm is to discontinue all incentives and support schemes for bioenergy and biofuels from 2020. This means that no more money will be spent in the implementation of political roadmaps to foster the bioeconomy – neither the energy use nor the material use of biomass. Instead, the market economy will be in charge of investment, production and distribution of biomass based on supply and demand. Six major advantages and disadvantages are listed below:

Advantages of abolishing incentives for bio-based energy

- No more political need to justify direct and indirect land use change (LUC and iLUC) or for certified sustainable feedstock, since the market would regulate the allocation of biomass and decide which products would be realised;

- Those bio-based products that create the highest added value will have a much better access to biomass;

- For the same reason, bio-based materials and products that can receive GreenPremium prices would be in favour (Carus et al. 2014b).

Disadvantages of abolishing incentives for bio-based energy

- An abrupt end of the support system endangers the majority of investments and employment in the bioenergy and biofuel sectors;

- Europe might not be able to realize its ambitious CO2 reduction goals;

- Sustainability requirements such as the protection of primary forests or working conditions will not be covered by legislation (as it is currently implemented in the RED) and thus not be implemented if any additional costs for the biomass are expected.

nova-Institute’s Recommendations

- Keep the existing infrastructure with a substantial reform of the RED. The existing infrastructures of bioenergy and biofuels, which are already under pressure, could be in danger after 2020. The current infrastructure is an advantage and forms the basis of the European bio-based economy. It should be used, preserved, and expanded by the transformation to bio-based chemicals and materials. To achieve this, nova-Institute recommends a substantial reform of the RED to a Renewable Energy and Material Directive (REMD), which will provide a level playing field for bio-based products. By promoting new material applications of biomass, more value added can be created per tonnes of biomass, new investments attracted and employment generated.

- Use mandates and bans to create environmentally friendly innovation. Mandates and bans should be used as strong instruments based on sound environmental and health reasons in order to tap the full positive potential of bio-based products. These market pull measures should be implemented in close coordination with a technological push in the form of support for R&D, pilot and demonstration plants and flagship investments, in order to get those technologies and products off the ground for which a sufficient market pull and demand exists.

- No limitation of R&D activities to specific biomass and applications only. R&D activities should be not limited to the conversion of lignocellulosic feedstocks, waste biomass and algae: research should also be conducted on the use of sugar beet in the chemical and plastics industry as well as the use of rapeseed oil in oleochemistry. Sugar is relevant because it is expected to become cheaper after 2017; rapeseed is relevant for keeping the existing infrastructure of the biodiesel industry, which is heavily under pressure, as well as biogas for electricity; biomethane has a relevant potential for the production of chemicals and polymers. Furthermore, the huge demand for cellulose fibre in textiles should not be ignored; it could be a great opportunity for the European pulp industry.

- Guarantee the supply security of high value industries. Overall, every development of the political framework for the bio-based economy should guarantee the supply security of high value industries such as chemicals and materials in order to prevent them from leaving Europe and taking their value and employment with them. The affordable access to biomass plays a crucial role in this.

References

Carrez, D. 2014: Sugar, Europe’s strength, in: Bio-based Press 2014-08-28 (http://www.biobasedpress.eu/2014/08/sugar-europes-strength/, last accessed 2014-09-15).

Carus, M. & Dammer, L. 2013: Food or non-food: Which agricultural feedstocks are best for industrial uses? Hürth 2013 (http://bio-based.eu/nova-papers).

Carus, M., et al. 2014a: Proposals for a Reform of the Renewable Energy Directive to a Renewable Energy and Materials Directive (REMD) – Going to the next level: Integration of bio-based chemicals and materials in the incentive scheme. Hürth 2014 (http://bio-based.eu/nova-papers).

Carus, M., Eder, A., Beckmann, J. 2014b: GreenPremium prices along the value chain of bio-based products. Hürth 2014 (http://bio-based.eu/nova-papers).

Martin, Michael J.C. 1994: Managing Innovation and Entrepreneurship in Technology-based Firms. Wiley-IEEE. p. 44. ISBN 0-471-57219-5.

OECD 2013: “Policies for Bioplastics in the Context of a Bioeconomy”, OECD Science, Technology and Industry Policy Papers, No. 10, OECD Publishing. http://dx.doi.org/10.1787/5k3xpf9rrw6d-en

Download policy paper, graphics and market pull list at www.bio-based.eu/policy

Source

nova-Institut GmbH, press release, 2014-10-01.

Supplier

Share

Renewable Carbon News – Daily Newsletter

Subscribe to our daily email newsletter – the world's leading newsletter on renewable materials and chemicals