The new report by nova-Institute presents a timely market analysis of China’s bio-based and biodegradable plastics industries and markets in 2024. On 71 pages, 14 tables, and illustrated by 13 graphics, the report provides an in-depth overview of the key products that dominate the Chinese market. It examines key market trends, policy dynamics, technological advances, key market players and growth opportunities. The aim is to provide chemical companies with actionable insights to navigate the Chinese market effectively and make informed decisions about market expansion or potential partnerships in China. In particular, the report highlights all relevant critical policies in the bio-based and biodegradable plastics markets since 2021 and in the future. It also provides first-hand market insights from Chinese entrepreneurs through in-depth face-to-face interviews with eight Chinese companies.

China: The world’s biggest plastics producer

In 2022, global plastics production reached 400.3 million tonnes, with a market value of 712 billion US$, an increase of about 1.6% since 2021. Asia is the world’s largest region for plastics production with a share of around 55%, of which China accounts for 32% with 128 million tonnes plastics in 2022.

Projected 49% CAGR growth of China’s bio-based plastics market until 2026

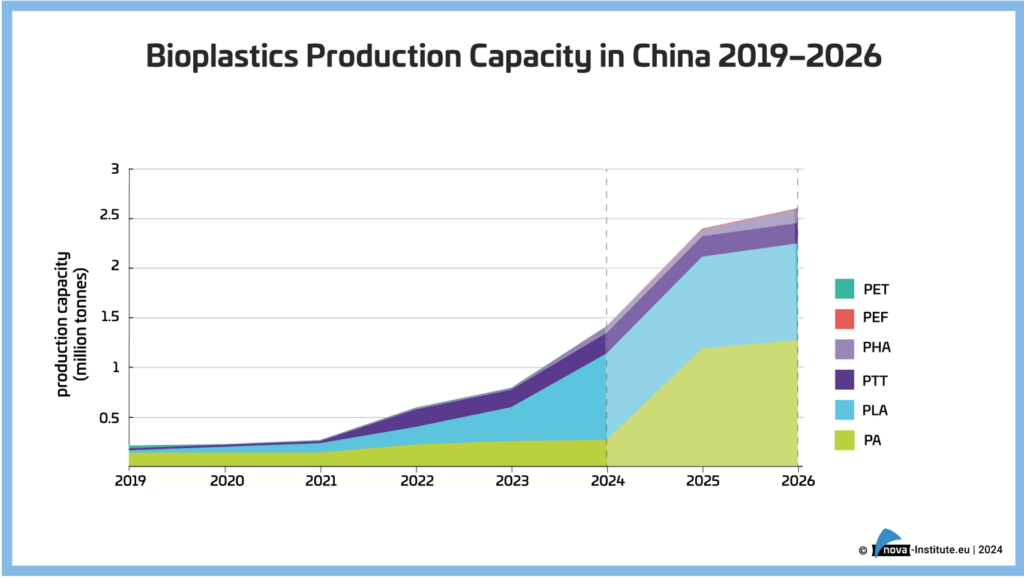

China’s bio-based plastics industry is experiencing rapid growth despite being in its early stages. This is largely driven by policy incentives. The industry is expected to expand significantly from 765,631 tonnes in 2023 to 2.53 million tonnes in 2026, representing a significant CAGR of approximately 49%.

Structural overcapacity in the biodegradable plastics market

Since 2020, the Chinese government has introduced a series of policies to boost the biodegradable plastics market, providing substantial resources and incentives to companies. Additionally, private equity firms have followed the policy trend by investing in this sector. These factors have contributed to industry growth but have also led to structural overcapacity.

In 2023, the combined annual production capacity of PLA and PBAT is 1.5 million tonnes, while the actual production is only 260,000 tonnes. Furthermore, the combined annual production capacity of PLA and PBAT is projected to reach 3.6 million tonnes by 2025, representing an average CAGR of 65%, but the market size is expected to increase to only 2.5 million tonnes by 2025. This suggests overcapacity in the biodegradable plastics market.

Chinese context: ‘Dual Carbon Goal’ in line with transformation policy

The Chinese government aims to promote the bio-based industry for two reasons. First, the government is committed to the carbon reduction goals outlined in the Paris Agreement. Second, it seeks to reduce its dependence on oil resources for national security reasons.

In 2020, China announced a new target to peak carbon dioxide emissions before 2030 and achieve carbon neutrality by 2060, commonly referred to as the ‘dual carbon target’. Current projections show that China’s CO₂ emissions are likely to enter a structural decline in 2024.

In addition, the Chinese petrochemical industry has embarked on a significant transition to a more sustainable model. China’s petrochemical industry is heavily dependent on imported oil. Projections indicate that the average external dependence between 2020 and 2030 will reach 76%, making it imperative for the Chinese government to take strategic action.

Key policies influencing the bio-based and biodegradable plastics industry

The new report by nova-Institute highlights the latest policies in China since 2021. One of the key policies unveiled in 2021 was the 14th Five-Year Plan for the Development of the Bioeconomy, which marked an important milestone in China’s national bioeconomy strategy. This plan prioritises innovation-driven development as its core principle and aims to build a national strategic force in biotechnology.

Following this strategy, the Chinese government has implemented a series of policies and regulations to promote the development of bio-based and biodegradable materials and chemicals, including the Three-Year Action Plan to Accelerate the Innovative Development of Non-Food Bio-based Materials, issued in 2023. This remarkable policy aims to make non-food bio-based products competitive with fossil-based products by 2050. The plan might have a profound impact on the future of the bio-based industry.

Key findings: Market drivers for China’s bio-based plastics industry

First, government incentive policies play a critical role. The Chinese government considers the bio-based industry as potentially supporting its ‘dual carbon’ plan, which has led to the implementation of various incentive policies and regulations in recent years.

Second, the presence of the existing chemical industry is significant. China’s well-established chemical industry has formed a complete value chain, enabling innovative bio-based start-ups to find partners to industrialise their products.

Third, the vast potential of the domestic market is a major driver for the bio-based industry. By 2026, the demand for bio-based plastics in China is expected to reach 2.53 million tonnes.

In addition, China has a relatively strong and active financing system, particularly in private equity (PE) and venture capital (VC). Although overall transactions in this sector weakened after 2020 due to the broader economic downturn in China, PE and VC remain active in emerging and strategic industries such as 5G, green energy and the bio-based industry.

The full version can be found here: https://renewable-carbon.eu/publications/product/bio-based-andbiodegradable-plastics-industries-in-china-pdf/

The short version can be found here: https://renewable-carbon.eu/publications/product/bio-based-andbiodegradable-plastics-industries-in-china-short-version-pdf/

More market and trend reports from nova experts

- ‘Bio-based Building Blocks and Polymers – Global Capacities, Production and Trends 2023–2028’

- ‘Mapping of advanced plastic waste recycling technologies and their global capacities’

- ‘Carbon Dioxide (CO₂) as Feedstock for Chemicals, Advanced Fuels, Polymers, Proteins and Minerals

- All can be found here: https://renewable-carbon.eu/publications/product/bio-based-and-biodegradable-plastics-industries-in-china-pdf/

About nova-Institut

nova-Institut GmbH has been working in the field of sustainability since the mid-1990s and focuses today primarily on the topic of renewable carbon cycles (recycling, bioeconomy and CO2 utilisation/ CCU).

As an independent research institute, nova supports in particular customers in chemical, plastics and materials industries with the transformation from fossil to renewable carbon from biomass, direct CO2 utilisation and recycling.

Both in the accompanying research of international innovation projects and in individual, scientifically based management consulting, a multidisciplinary team of scientists at nova deals with the entire range of topics from renewable raw materials, technologies and markets, economics, political framework conditions, life cycle assessments and sustainability to communication, target groups and strategy development.

50 experts from various disciplines are working together on the defossilisation of the industry and for a climate neutral future. More information at: nova-institute.eu – renewable-carbon.eu

Source

nova-Institute, press release, 2021-05-31.

Supplier

nova-Institut GmbH

The State Council of the People's Republic of China

Share

Renewable Carbon News – Daily Newsletter

Subscribe to our daily email newsletter – the world's leading newsletter on renewable materials and chemicals